By Rishi Shah and Neel Shah

FUEL RIOTS

A statue of Marianne, vandalised inside the Arc de Triomphe in protest

Violent riots have gripped the streets of France due to the high cost of living in Paris. The “Yellow Jacket” protestors are voicing their concerns over the high cost of fuel in Paris. This is in retaliation to the increase in the fuel taxes by the President Emmanuel Macron. France, unlike the UK, haven’t frozen fuel duty, and hence it increases annually. This means that as fuel is an essential expenditure for the majority of the population, it is directly increasing cost of living and people are rendered worse off.

The counter argument, and the pretence held by the President, is that his fuel policies are needed to combat global warming. This movement has also grown through French social media networks and it now includes rising anger at high taxes and living costs, and wider criticism of President Macron's economic decisions.

How significant have the tax increases been? The price of diesel, which is France is the most commonly used fuel for cars, has risen by around 23% over the past year to an average of €1.51 per litre. This is one of the highest prices since the beginning of the 21st century. Although world oil prices have risen recently, they are currently plummeting to record lows, however, French hydrocarbon tax was increased by 7.6 cents per litre on diesel and 3.9 cents on petrol, as part of a drive for cleaner and environmentally friendly cars and fuel. Recently, it was the government also decided to impose a further increase of 6.5 cents on diesel and 2.9 cents on petrol, to come into fruition by 1 January 2019 and this was the final straw for the French public. It has evolved into 3 weeks of incessant riots.

BREXIT: DOOMED TO FAILURE?

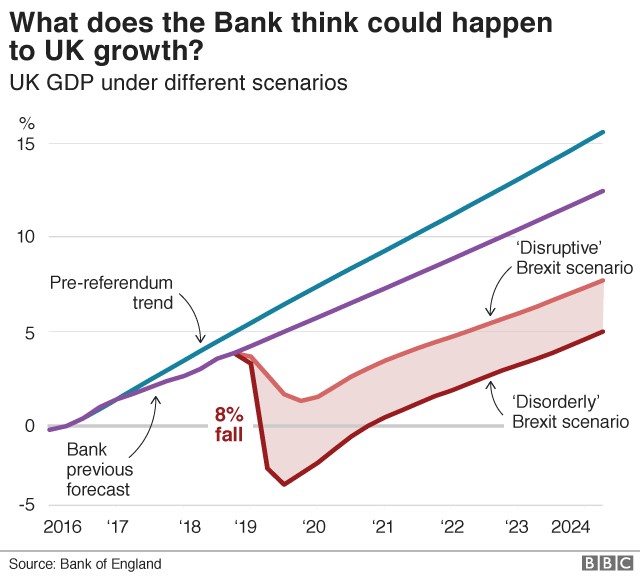

Figures from the UK government and the Bank of England have suggested that under Theresa May’s Chequers deal, the economy will be 3.9% smaller after 15 years, in comparison with remaining in the European Union. However, this is much less significant than the potential 9.3% hit to the UK economy from a no-deal Brexit. The 3.9% is estimated to be approximately £100bn, a significantly larger cost in comparison to the costs of the EU stated prior to the vote.

However, former Brexit Secretary, David Davis, has questioned the validity of the research by the Treasury. This includes ignorance over the potential benefits of new trade deals strung with the rest of the world.

In addition, the deal does not consider regional differences. For example, research has shown that a no-deal situation will leave London with the least damage, hitting the North East and West Midlands. However, the government’s option for Brexit will hit the capital the hardest.

The Bank of England has also had a similar forecast, despite being independent form government influence. However, the Bank suggests an immediate hit, rather than a long-term impact.

HOUSING DEMAND FALLS AMID BREXIT UNCERTAINTY

Estimates from both Nationwide and Halifax has shown that housing demand has been subdued as a result of scepticism over the effects of Brexit. This led to a five-year low in housing price increases in October, at only 1.6%. This is particularly true in London, where the ongoing housing boom has slowed and levelled, appearing to remain so for the next few years.

Housing is a major purchase, however, with demand subdued, house prices have taken a hit. Affordable housing is rare, particularly in the south-east, however, will Brexit lead to falls in house prices in areas like London?

PROGRESS AT THE G20 SUMMIT

The G20 summit, held in Argentina over the weekend, showed signs of international progress as the US-China trade war could be ending. Mr Trump and Mr Jinping, the respective leaders of US and China, reached a deal to hold off on the proposed tariffs that they both had lined up. Hopefully, this will remove the fire from the trade war and stabilise the financial markets.

The deal that was reached is as follows: The USA will not increase tariffs on $200bn of Chinese goods from 10 per cent to 25 per cent in January, which was what had been planned. China meanwhile would move to purchase a “very substantial” volume of farm, energy and industrial goods, in order to reduce the trade gap (difference between imports and exports between the two nations) with the US. There will be further negotiation in order to solve the other issues that Trump has with China, such as intellectual property theft and the forced transfer of technology, with these talks having a deadline of three months.